Finding ways to improve cash flow is tricky in the best of times, and it is particularly so in this era of rising costs and rapid technology adoption. However, as a fractional CFO who works with growth-minded CEOs across industries, let me assure you – there are always opportunities if you know where to look.

Cash flow issues are stressful, but once you understand the basics (and apply some discipline), they become easier to manage. Below, I explain how to improve cash flow in a business and where to tweak your approach to account for industry nuances or a changing economy.

Table of Contents

What is Cash Flow?

“Cash flow” refers to the net amount of money flowing in and out of your business over a given period. If your net cash flow is positive, it means you are generating enough liquid funds to run your company, meet your financial obligations, and invest in the business. If it is negative, you are at risk and must take steps to remedy the situation.

Cash flow is not the same as profitability. If you generate more revenue in a month than you spend on revenue-generating activities, you are profitable. But if you must wait 30, 60, or even 90 days for customers to pay, you can still face cash flow problems. So, what can you do about it?

The No-BS Financial Playbook for Small Business CEOs

Are you tired of making costly financial mistakes? Stop guessing and start growing. Learn how to create a scalable and valuable company while minimizing risk with this playbook from a serial entrepreneur who has been in your shoes.

How to Improve Cash Flow: 8 Actionable Tips

Improving cash flow requires strong financial management practices combined with initiatives to increase cash inflows and reduce cash outflows. I organized the tips below into these three areas.

Strengthen Financial Management

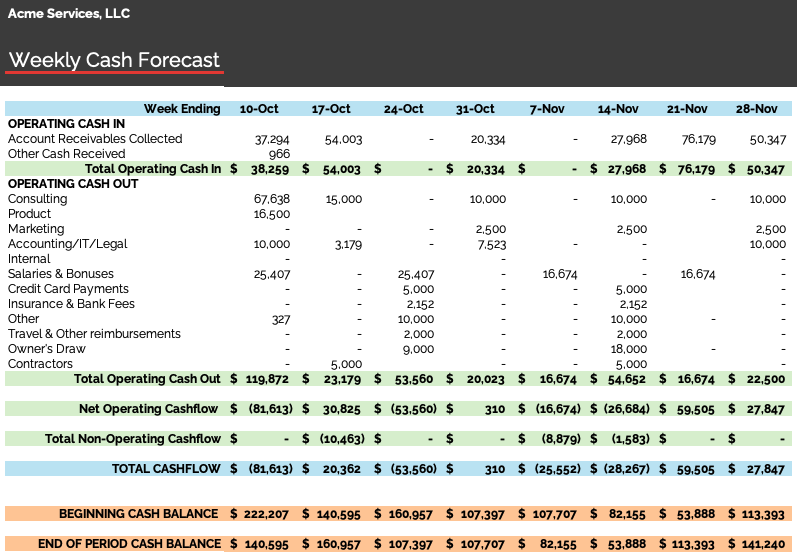

1. Build a Cash Flow Forecast and Use it Regularly

The first thing we recommend you do, and what we do when working with clients, is to build a detailed cash flow forecast.

A cash flow forecast starts with your cash position today. Then you project forward based on your expected revenues and expenses. It provides visibility into your cash situation each month, or even week, if that’s what your business requires, and empowers you to test scenarios. It allows you to spot positive or negative cash flow before it occurs and take steps to optimize the situation.

Your cash flow forecast must show the breakdown of all cash sources and uses – cash flows from operating, investing, and financing activities. The goal is to create a healthy cash flow situation where you have the funds you need when you need them. For that, you need complete transparency.

Here are the basic steps in cash flow forecasting:

- Start with an analysis of your current cash position (i.e., all the cash you have in your bank account(s)). You will also need current, detailed versions of your accounts receivable and accounts payable aging reports.

- Map out expected cash coming in (customer payments, timing of collections) and going out (payroll, vendor payments, operating expenses) for the next 12 months. Add one-time or extraordinary cash payments (or receipts) like equipment purchases, loan payments, tax obligations, or planned investments. Build a running total that shows your projected cash position week by week or month by month, highlighting when you will be tight or flush.

- Run scenarios for what happens if customers pay more slowly, a big deal falls through, or unexpected expenses hit.

Once you have your forecast, use it to manage your cash flow proactively. Compare your company’s performance each month against your forecast, then make any necessary adjustments to stay on track.

2. Use Debt Strategically

Although it’s certainly preferable (and less stressful) to run your business debt-free, please keep an open mind, especially when you’re trying to decide how to increase cash flow. In short, debt financing is fine if you can afford it, meaning you can comfortably service both the debt and the interest. That makes this one of those areas where you must pay close attention to economic factors (i.e., be mindful of changing interest rates).

Use your cash flow forecast to model the impact of a loan on your current and future cash flows. That will help you see how long it will take to pay off your debt and how the funds will affect your ability to drive revenue, making this decision easier.

Whether debt comes in the form of credit cards, a line of credit from a financial institution, or even long-term loans from friends and family, be sure to clarify the terms. Secured loans (based on the company’s assets or a personal guarantee) are much less expensive (3%-4% interest rates) than unsecured loans. Unsecured loans can range from 6% to 8% for bank loans to 25% to 35% for non-traditional lenders.

Avoid any lender with oppressive performance terms and conditions that would put your business at risk. If you are unsure about what is best for your situation, ask a professional.

Increase Cash Inflows

3. Build a Strong Receivables Management Process

It’s surprising how many companies don’t have a good process for collecting payments. I’ve seen service-based businesses, for instance, that do fantastic work for their clients, but bill in arrears and then fail to follow up on late payments. Clearly, this will inhibit your quest to create positive cash flow.

Therefore, we recommend developing a rock-solid, repeatable process for accounts receivable management. That typically involves:

Investing in Invoicing and Accounting Software

If you don’t have a solution (like QuickBooks) for managing your finances or if you’re not using its features to keep your receivables current, it’s time to invest. In addition to tracking business cash flow, these solutions make it easier (and faster) to create and send invoices, set up electronic payment processing, and follow up when a client’s bill is past due.

Imposing Penalties for Late Payments

Many clients will pay at the last minute (or even late) if there is no incentive to pay on time. That can harm your bottom line. Setting clear payment due dates and late-payment penalties (1.5% per month, or 18% annually) will discourage this behavior.

Although this may feel unnatural at first, you will get into a groove, and your clients will understand that it is a necessary part of doing business.

4. Develop Early Payment Strategies

Anything that allows you to receive payments sooner is a great way to improve cash flow. Here are a few ways to do that, but there may be others specific to your industry.

Credit Cards

Many companies prefer to pay by credit card. Offering that as an option could mean receiving payment within 2-3 days, rather than a month or more when paid by check. The credit card company will charge a 3% transaction fee, but you can often pass that to your customers, significantly improving cash flow.

Pre-Payment Discounts

Pre-payment discounts benefit both parties. The customer gets a deal for early payment, you get cash to run your business, and you reduce the time spent chasing late payments.

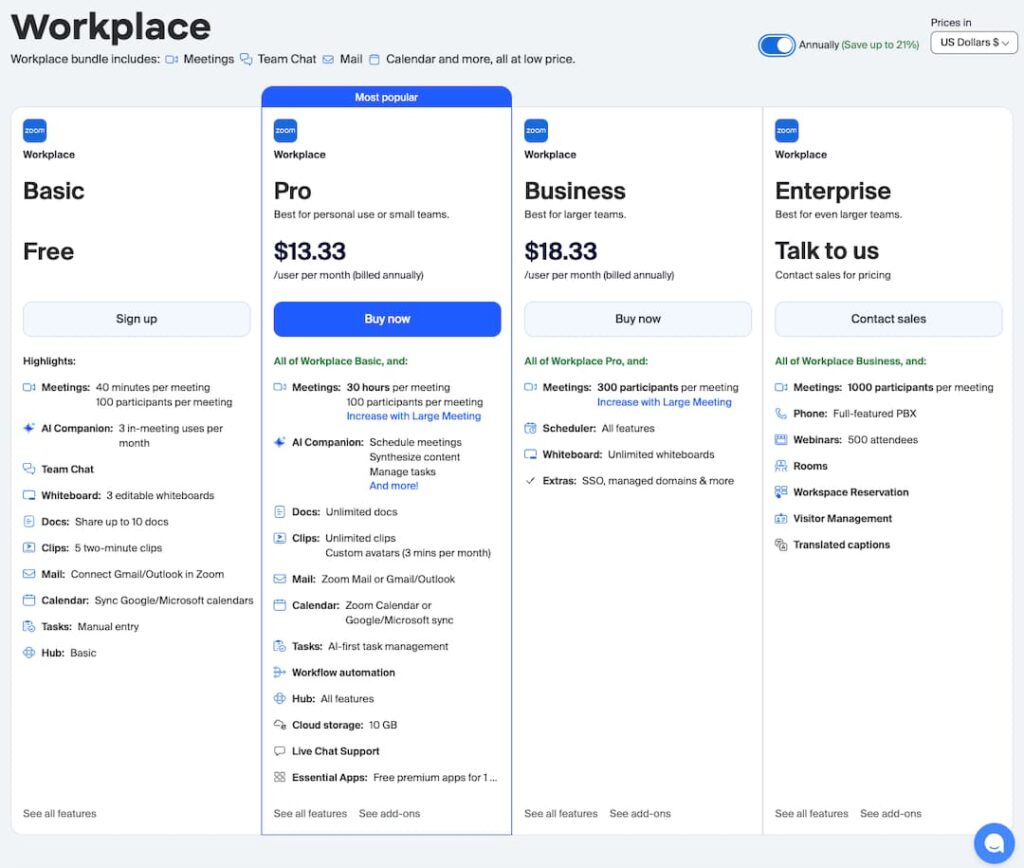

You’ve undoubtedly seen this in practice with companies like Zoom. Customers can pay monthly or get a reduced rate by paying for an entire year of service up front.

This model works well for recurring-revenue services, but it is also effective with other types of products or services. For example, you may have heard of “2 net 10” or “2/10 net 30” payment terms. Under these terms, if your customer buys $10,000 worth of widgets and pays within 10 days, they get a 2% discount, and you get $9,800 roughly 20-25 days sooner than the standard “net 30” terms.

Invoice Factoring

Invoice factoring is when you bill customers as usual, then sell the invoice to a third party. You get the working capital today, and the third party assumes the risk of non-payment for a small fee (typically 1%-2%).

5. Sell Ancillary Services

Expanding your offering is an exciting way to increase cash flow and generate more revenue. For example, imagine you manufacture and sell widgets used to produce larger products. You could offer consulting services to customers who need help integrating the widgets into their product lines. This service would help your customers deliver more cost-efficient products and allow you to charge more.

Of course, it’s important to avoid overextending yourself. Focus on products or services that complement your current offering to avoid straying too far from your core competency. Also, since cash flow is a concern, steer clear of anything that would add costs you can’t easily absorb. Other ideas for the widget manufacturer include extending the product line by offering related products or expanding into another market using the same product line.

6. Increase Prices and Fees

When exploring how to improve cash flow, you must consider pricing. If your products or services are underpriced, or you haven’t raised your rates in several years, it may be time to increase them. Or enhance your current offering to justify charging more.

I understand that this is a delicate topic, especially during economic downturns. If you’re in a competitive space, you can’t afford to price yourself out of the market. And you certainly don’t want to scare off loyal customers with a significant cost bump. But if you can justify the increase, it’s worth exploring.

Most customers will find an increase reasonable if you haven’t raised your rates in years or if you must cover unexpected costs, as long as you are transparent in your communications. Explain that you value their business but must occasionally increase your rates to keep up with rising costs.

Control Cash Outflows

7. Renegotiate Terms with Vendors and Suppliers

One of the most impactful ways to increase cash flow is to renegotiate vendor and supplier contracts, thus reducing your operating expenses. While it may not be possible with everyone, a quick review of your records might unearth some opportunities. Here are a few examples that you can expand upon, depending on your industry or economic factors.

Rental Agreements

Just because you have a lease doesn’t mean you can’t request a change. For instance, if you are two years into a 5-year lease that’s running you $10,000 per month, you could offer to extend the lease for 1 year in exchange for a 10% rent reduction.

Supplier Terms

If you have a supplier you use all the time (and you’re in good standing), look for ways to get a cost break. Some suppliers will offer discounts or waive shipping fees in exchange for a larger order, even if they must send the items over time.

Utility Providers

Many utility providers will give existing customers their best available rates, but only if you ask. For example, if your cell phone provider reduces your rate by $10 per month, per line, that can have a significant impact at scale.

The trick with any of these scenarios is to come to the table prepared to make an offer. Review your records and perform research to gather comparable data. Then make your case in the spirit of creating a win-win. Explain that you’re a good customer and want to continue the relationship, but you need something in return.

8. Eliminate Non-Essential Expenses

Overlooking excess expenses is easy when things are going well. You no longer have this luxury when experiencing cash flow problems. Seek ways to increase cash flow by going through your expenses with a fine-tooth comb and removing fluff.

That isn’t as painful as it sounds; there are often some easy opportunities that become apparent as you build your cash flow forecast. Here are some common ones.

Hiring Fractional Help vs. Full-Time Employees

Do you genuinely need full-time employees, or would fractional help suffice? We often help clients build entire teams this way, initially hiring part-time help, then moving to full-time as the company grows. Download our “Building a Winning Team” guide to see how it works, even for executive roles.

Investments That Can Wait

Consider delaying technology upgrades, research and development, trademark legal fees, or even hiring plans. But do not postpone safety upgrades that could leave your business at risk.

Professional Development or Training Expenses

While important, you can defer some training and development expenses. That will provide some relief when you are short on cash.

Unnecessary Travel and Meal Expenses

Although some travel may make sense, this is a significant area of waste for many organizations. Make wise choices and establish travel expense reimbursement policies to reduce costs.

Employee Perks

Your employees may grumble if you cut perks like gym memberships, company-sponsored happy hours, and expensive snacks. But they will quickly come around if you explain that you must improve cash flow and see downsizing or cutting salaries as a last resort.

Leasing Equipment or Property vs. Buying

Although leasing costs more in the long run, the payments are typically lower. That makes it a viable option for businesses concerned about cash flow.

The Benefits of Improving Cash Flow

Improved cash flow gives you peace of mind and makes it easier to manage your company’s financial obligations day-to-day. But that’s just a start. Building a rigorous cash flow forecasting process, establishing safeguards, and using them religiously takes this to the next level. It allows you to spot and address problems before they spin out of control and empowers you to make confident, impactful business decisions that fuel growth.

At The CEO’s Right Hand, we help clients diagnose and resolve financial challenges, such as increasing cash flow, daily. Read “Cash Flow Forecasting: A Business Owner’s Guide” or download one of our resources to learn more, or reach out to request a chat.

Editor’s Note: This blog post was originally published in December 2020 and then updated for accuracy and thoroughness in December 2025.